The TC Venue regime may also become relevant to UK platform operators in light of the UK’s vote to leave the European Union (known as Brexit).

MiFID II will also introduce a mandatory trading requirement for equities, which we will cover separately in a later alert.

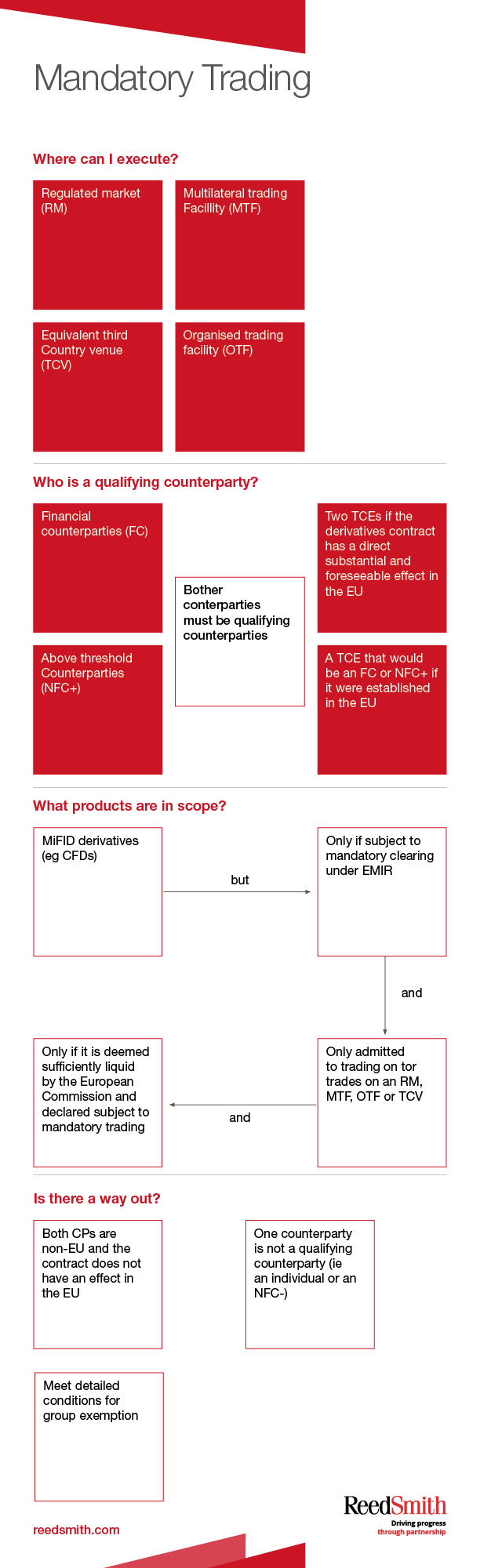

This diagram contains an overview of the Trading Requirement.

What?

The Trading Requirement is potentially applicable to all derivatives within the scope of MiFID, but only where the derivatives asset class: (a) has been declared subject to mandatory clearing under the European Markets Infrastructure Regulation (EMIR); (b) is traded or admitted to trading on at least one Relevant Trading Venue; and (c) is considered by the European Commission to be sufficiently liquid to trade only 'on venue'.

Who?

The Trading Requirement will apply when both counterparties to the derivatives contract are “qualifying counterparties” (i.e. financial counterparties (FCs) and above threshold counterparties (NFC+s) as defined in EMIR). So the Trading Requirement applies when FCs and NFC+s trade with each other and when they trade with non-EU counterparties who would be treated as an FC or an NFC+ if established in the EU.

The Trading Requirement will also apply to derivatives entered into between two non-EU counterparties where those trades have a "direct, substantial and foreseeable effect" in the EU or where the Trading Requirement should apply in order to prevent the evasion of the Trading Requirement.

Way out?

A derivatives trade that involves an individual or a below threshold undertaking (i.e. an NFC) will fall outside the scope of the Trading Requirement.

There is an exemption for “group transactions” provided that certain conditions are satisfied. It is important to note, however, that where the qualifying counterparty is based outside of the EU, the European Commission must have adopted an equivalence decision in relation to the regulatory framework of the non-EU jurisdiction.

What does this all mean?

It remains unclear what derivative products ultimately will be declared subject to the Trading Requirement; however, a Discussion Paper issued by ESMA on 20 September 2016 considers the trading obligation for derivatives. The paper concentrates on those products which have already been declared subject to mandatory clearing under EMIR (certain Interest Rate Derivatives and certain Credit Derivatives). It appears unlikely that equity derivatives, FX non-deliverable forwards and forward rate agreements will be subject to the Trading Requirement at the outset but it is possible that the Trading Requirement could eventually cover these products. Counterparties and platform operators should assume that more MiFID derivatives could be in scope and plan accordingly to ensure that they will be in a position to comply with the Trading Requirement when it comes into force.

This may mean that firms that operate as an SI may have to stop trading derivatives within the scope of the Trading Requirement or restructure their existing “bilateral” trading arrangements.

In order to retain European business, a platform operated by a firm based outside of the EU will need to consider whether it has to establish an entity in the EU that qualifies as a Relevant Trading Venue or whether it qualifies as a TC Venue. The latter requires the European Commission to issue an equivalence decision in relation to that third country's legal and supervisory framework (e.g. against MiFID II and the market abuse regulation (MAR)), and the operator must be authorised and supervised in its home state (the Equivalence Route). It is important to note that equivalent status is only relevant for the purposes of the Trading Requirement.

A third country’s legal and supervisory framework will be deemed to be equivalent where:

- the trading venue is authorised and subject to effective supervision and enforcement in its home state on an on-going basis;

- the trading venue has clear and transparent rules regarding admission of instruments to its platform and they are capable of being traded in a fair, orderly and efficient basis and are freely negotiable;

- issuers of instruments in that third country are subject to periodic and on-going information requirements ensuring a high level of investor protection;

- the third country ensures market transparency and integrity via rules addressing market abuse in the form of insider dealing and market manipulation; and

- the third country must have an effective equivalent system in place for the recognition of trading venues authorised under foreign regimes to request access to CCPs established in that third country.

Post-Brexit

On the assumption that the UK will still be a member of the EU on 3 January 2018, a UK authorised operator of an RM, MTF and OTF will still be recognised as a Relevant Trading Venue on 3 January 2018. Associate membership of the EU (e.g. on a Norwegian basis) would also produce a similar outcome for UK platform operators.

In the event that the UK is treated as a third country post-exit, a UK operator of an RM, MTF and OTF may still qualify as a Relevant Trading Venue under the Equivalence Route. Provided that the UK continues to apply MAR and that it implements and retains MiFID II post-exit then it is likely that the UK’s legal and supervisory framework would be deemed to be equivalent by the European Commission, although the precise timing of such an equivalence decision would be unknown.

It is important therefore for UK platform operators actively to engage with industry bodies in any lobbying efforts to ensure that a sensible outcome is reached in the ”exit” negotiations to ensure continued access to the single market.

What questions do I need to ask?

Counterparties

- Do I trade in derivatives within the scope of MiFID?

- Have the derivatives I enter into been declared subject to mandatory clearing under EMIR?

- How am I categorised (e.g. an FC, NFC+ - see our Please see our earlier Technical Update for further details on counterparty classification)?

- How is my counterparty categorised?

- Do I currently execute those derivatives trades on an RM or an MTF? If so, where are those venues established? Will I have access to an RM, MTF, OTF or TC Venue once Mandatory Trading applies?

Platform operators

- Does the platform that I operate permit trading in derivatives within the scope of MiFID?

- Have those derivatives been declared subject to mandatory clearing under EMIR?

- How are the liquidity providers and users of my platform categorised?

- Am I a multilateral platform or a single dealer platform?

- What is my current regulatory status?

- Do I need to restructure my arrangements, including in light of Brexit?

- Do I need to become authorised?